Qualifying Year

Qualifying year refers to the year for which Wage Credit Scheme payout is computed, based on the wage increases given in that year. There are 9 qualifying years - 2013, 2014, 2015, 2016, 2017, 2018, 2019, 2020 and 2021.

Qualifying Employer

All employers, except for the following entities on the employer exclusion list, will automatically qualify if they pay qualifying wage increases to their Singaporean employees:

Employer Exclusion List

- Local Government Agencies including Organs of State, Ministries and Departments, Statutory Boards

- Government and Government-Aided Schools

- PA Services and Grassroot Units

- High Commissions, Embassies, Trade Offices, Consulate

- Unregistered Local/Foreign Entities

- Foreign Military Units

- Representative offices of Foreign companies, Foreign Government Agencies, Foreign Trade Associations/ Foreign Chambers/ Foreign Non-profit Organisations/Foreign Law Practices

- Bank Representative Offices/Insurance Representative Officers/Other Financial Representative Offices (registered with MAS); News Bureaus (which are representative offices);

- International Organisations

- Entities which pay CPF but are not registered in Singapore

Qualifying Employee

- A Singapore Citizen;

- Earning a gross monthly wage less than the Gross Monthly Wage ceiling*; and with a minimum gross monthly wage increase of $50 in the qualifying year;

- Received CPF contributions from a single employer, for at least three calendar months in the preceding year;

- On employer's payroll for at least three calendar months in the qualifying year (i.e. employer must have paid employee CPF contributions for at least three calendar months in qualifying year)

- Must not also be the business owner of the same entity (i.e. sole proprietor of the sole proprietorship, or a partner of the partnership, or both a shareholder and director of a company)

*In Budget 2020, the qualifying gross wage ceiling was raised from $4,000 to $5,000 for 2019 and 2020.

*In Budget 2021, the Scheme was further extended for one more qualifying year to cover 2021 wage increases. The qualifying gross wage ceiling remained at $5,000.

Additional Eligibility Conditions

- An employer is not eligible for a payout under any of the circumstances below:

- The employer is an entity that has no substantial trade or business;

- The employer had given, in IRAS' opinion, false or misleading information to IRAS in order to obtain a payout or a higher amount of payout;

- The employer (either singly or with another person) had used, in IRAS' opinion, one or more artificial, contrived or fraudulent steps in order to obtain a payout or a higher amount of payout;

- The employer was convicted in the qualifying or preceding year for making CPF contributions to Singaporeans who were not actively employed by the firm

- An employer is not eligible for a payout for a wage increase for a particular employee who:

- Did not carry out any substantive work for the employer;

- Effectively controls the employer (i.e. controls decision making power and management of the business or company)

- If the total wages paid by an employer for a period is not commensurate with the volume or nature of activity carried out by the employer in that period, then the employer is only eligible for an amount of payout that, in IRAS' opinion, corresponds to the increase in the total wages paid for that period that commensurate with such volume or nature of activity.

- If the total wages paid by an employer to a particular employee for a period is not commensurate with the volume or nature of work carried out by the employee in that period for the employer, then the employer is only eligible, in respect of that employee, for an amount of payout that, in IRAS' opinion, corresponds to the increase in the total wages paid to that employee for that period that is commensurate with such volume or nature of work.

- If an employer fails to give to IRAS, by the time specified by the IRAS, any information requested by IRAS for the purpose of determining the employer's eligibility for a payout or the amount of payout the employer is eligible for, with respect to one or more employees, then the employer will not be given the payout for these employees.

Qualifying Wage Increase

- Qualifying wage increase refers to the amount of wage increase of the employee that qualifies for co-funding in any qualifying year. It constitutes the gross monthly wage increase given in any qualifying year and the sustained gross monthly wage increases

given in preceding years.

- Gross monthly wage increases of at least $50 in the qualifying years 2018 and 2019 will qualify for 20% co-funding up to the Gross Monthly Wage level of $4,000, while the wage increases in the qualifying years 2020 and 2021 will qualify for 15% co-funding, up to the Gross Monthly Wage level of $5,000 from 2020 and 2021. In addition, gross monthly wage increases (at least $50) previously given in 2017, 2018 and 2019 by the same employer will continue to be co-funded at the respective levels of co-funding if they are sustained in 2018, 2019 and 2020.

- With the Scheme extension to qualifying year 2021, gross monthly wage increases (at least $50) previously given in 2019 and 2020 by the same employer will continue to be co-funded if they are sustained in 2020 and 2021.

- Once an employee's gross monthly wage exceeds $5,000, the portion of the wage increase that brings the gross monthly wage above $5,000 will not be eligible for co-funding.

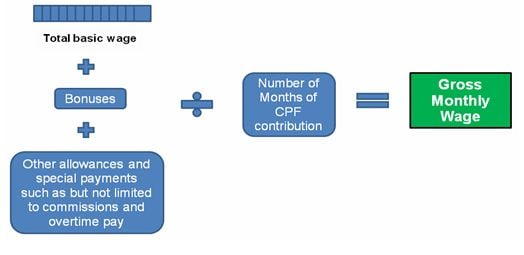

Gross Monthly Wage

Gross Monthly Wage is defined as the total wages paid by the employer to the employee in the calendar year, divided by the number of months in which CPF contributions were made.

Total wages includes all allowances and payments that attract CPF contributions, including basic salary, overtime pay, commissions and bonuses. Total wages excludes employer CPF contributions.