Taxes for nation-building

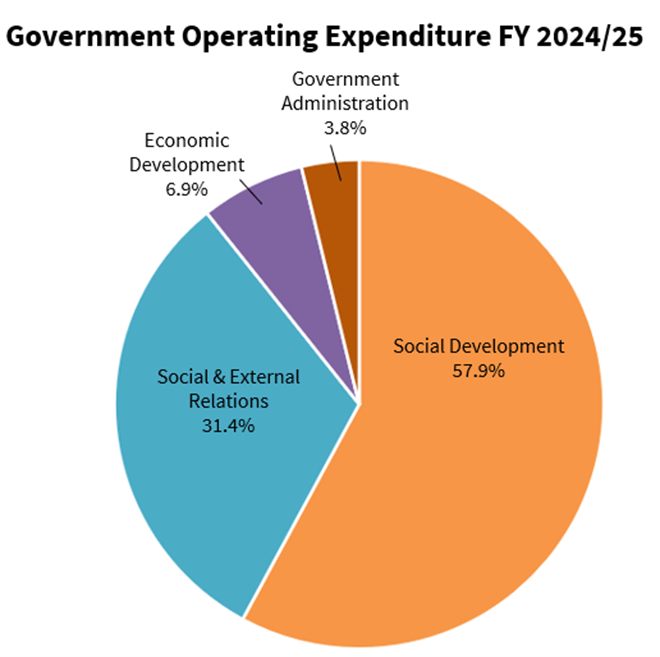

Taxes support the Singapore government's spending on public goods and infrastructure that enable our people and businesses to thrive and grow. In the fiscal year 2024/25, most of the Government Operating Expenditure (57.9%) was channelled towards improving people's lives (Social Development). The next largest share (31.4%) was spent on areas such as Defence, Home Affairs, and Foreign Affairs (Security & External Relations). The rest (6.9% and 3.8%) went towards growing the economy and government administration respectively.

Source: Economic Survey of Singapore, Second Quarter 2025

Fiscal policy

Fiscal policy in Singapore is how the government collects and uses revenue to influence the economy. The main goals are to:

- Create the conditions for macroeconomic stability,

- Support economic growth and

- Promote social equity.

This is done through maintaining a balanced budget, investing for the future, and ensuring a fair and progressive fiscal system that fosters social mobility.

Tax policy

Tax policy in Singapore serves two main purposes:

- Revenue Raising

Taxes are a key source of funding for government operations. - Promotion of Economic and Social Goals

Taxes are used to influence behaviour for desirable goals. For example, encouraging businesses to innovate and internationalise, and families to have more Singaporean children.

Singapore relies on a combination of direct taxes and indirect taxes to fund Government expenditure and promote economic and social objectives such as having an overall progressive system of taxes and transfers.

Government operating revenue

The main sources of government operating revenue are tax revenue, fees and charges, and other receipts. Tax revenue administered by IRAS accounts for 76.9% of the government operating revenue for the fiscal year 2024/25. This includes:

- Income Tax

Income tax is chargeable on the income of individuals and companies. - Goods & Services Tax (GST)

GST is a tax on consumption. The tax is paid when money is spent on goods or services, including imports. - Property Tax

Property tax is imposed on owners of properties based on the expected rental values of the properties. - Stamp Duty

This is imposed on commercial and legal documents relating to stock & shares and immovable property. - Gambling Duties

These are duties on betting, lotteries, sweepstakes, and gaming machines in any non-casino premises. - Casino Tax

The casino tax is a tax levied on the casinos’ gross gaming revenue. - Estate Duty (Removed for deaths occurring on or after 15 Feb 2008)

Estate duty is levied on the value of a deceased's net assets in excess of a threshold amount.

IRAS is implementing the Income Inclusion Rule and the Domestic Top-up Tax under Pillar Two of the Base Erosion and Profit Shifting (BEPS) 2.0 initiative, for in-scope multinational enterprise groups for financial years starting on or after 1 Jan 2025 under the Multinational Enterprise (Minimum Tax) Act:

- Multinational Enterprise Top-up Tax (MTT)

MTT is chargeable on a parent entity located in Singapore in respect of the profits of the group entities operating in any jurisdiction outside Singapore where the jurisdictional effective tax rate of such entities is less than 15%. - Domestic Top-up Tax (DTT)

DTT is chargeable on a local filing entity in respect of the profits of the group’s entities operating in Singapore where the effective tax rate of such entities is less than 15%.

Other taxes imposed by the government and administered by other government agencies include:

- Customs, Excise, and Carbon Taxes

- Motor Vehicle Taxes

- Vehicle Quota Premiums

- Fees and Charges (Excluding Vehicle Quota Premiums)