Under the Rental Relief Framework, owners (i.e. landlords) of qualifying non-residential properties would have received a cash grant. The cash grant is not taxable.

Landlords are required to provide rental waivers to eligible tenants through any of these methods:

Monetary payments to the tenants; and/or

Reduction of rent or licence fee provided to the tenant; and/or

Passing on the Property Tax Rebate to the tenants, fully or partly.

To simplify YA 2021 income tax reporting, landlords who are individuals may report the reduced amount of rental income as the gross rent.

Below are illustrations of 4 common scenarios showing how tax reporting on the rental income can be made for the YA 2021, assuming that the landlord has fulfilled the rental waiver obligations under the law in 2020.

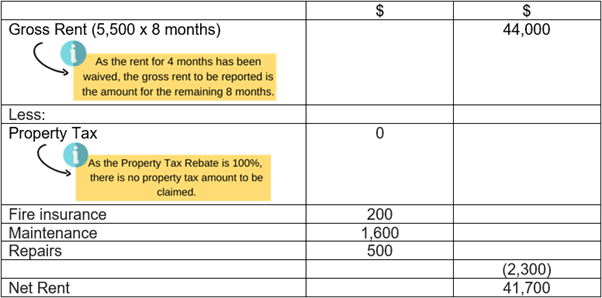

Scenario 1 - Landlord passed on part of the 100% Property Tax Rebate to the tenant of a retail shop

Period of rental: 1 Jan 2020 to 31 Dec 2020

Rental per month: $5,500

Property Tax: $6,000

Property Tax Rebate received : 100% of $6,000

Amount of Property Tax Rebate passed on to tenant: $5,000

- In this scenario, tenant qualified for 4-month rental waiver i.e. $5,500 x 4 = $22,000

- As the landlord has passed on the Property Tax Rebate of $5,000 to tenant, he has waived a further amount of $17,000 (i.e. $5,500 x 4 - $5,000) of rent for year 2020, making it a total of $22,000.

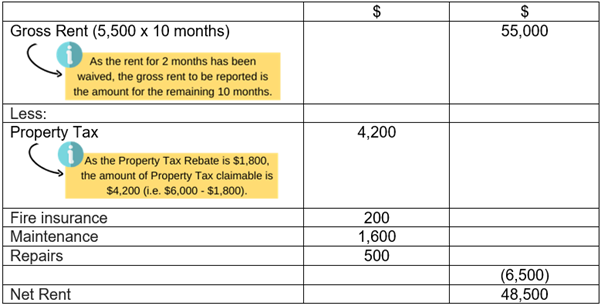

Scenario 2 - Landlord passed on full 30% Property Tax Rebate to the tenant of an office

Period of rental: 1 Jan 2020 to 31 Dec 2020

Rental per month: $5,500

Property Tax: $6,000

Property Tax Rebate: 30% of $6,000 i.e. $1,800

Amount of Property Tax Rebate passed on to tenant: $1,800

- In this scenario, tenant qualified for 2-month rental waiver i.e. $5,500 x 2 = $11,000

- As the landlord has passed on the Property Tax Rebate of $1,800 to tenant, he has waived a further amount of $9,200 (i.e. $5,500 x 2 - $1,800) of rent in 2020, making it a total of $11,000.

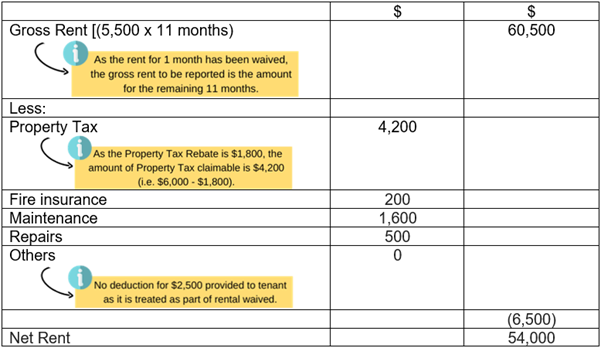

Scenario 3 - Landlord passed on full 30% Property Tax Rebate and provided monetary payment to the tenant of an office

Period of rental: 1 Jan 2020 to 31 Dec 2020

Rental per month: $5,500

Property Tax: $6,000

Property Tax Rebate: 30% of $6,000 i.e. $1,800

Amount of Property Tax Rebate passed on to tenant: $1,800

Amount of monetary payment provided to tenant: $2,500

- In this scenario, the tenant qualified for 1-month rental waiver i.e. $5,500

- As the landlord has already passed on the Property Tax Rebate of $1,800 and provided monetary payment of $2,500 to tenant, he has waived a further amount of $1,200 (i.e. $5,500 - $1,800 - $2,500), making it a total of $5,500

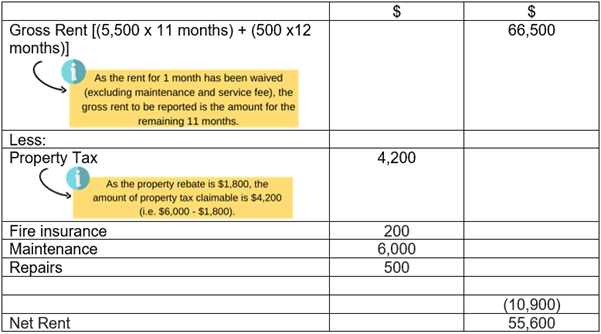

Scenario 4 – Tenant of an office still has to pay the maintenance & service fee as they are not waived; landlord did not pass on Property Tax Rebate to the tenant

Period of rental: 1 Jan 2020 to 31 Dec 2020

Rental per month: $6,000 (including $500 for monthly maintenance and service fee)

Property tax: $6,000

Property tax rebate: 30% of $6,000 i.e. $1,800

- In this scenario, the tenant qualified for 1-month rental waiver (excluding maintenance and service fee) i.e. $6,000 - $500 = $5,500

- The landlord did not pass on the Property Tax Rebate $1,800 to tenant, he has waived the 1-month rental of $5,500.