Module 2: Charging GST on Supplies – Standard-Rate

Learning Objectives:

• When are supplies zero-rated?

• When do international services qualify to be zero-rated?

• When do exports of goods qualify to be zero-rated?

• What is the Major Exporter Scheme?

On this page:

Charging GST on Supplies – Zero-Rate

Learn about when to charge 0% GST on international services and exports of goods.

Learning Activity - Test Your Understanding

Q1. For an international service to be zero-rated, it must fall within the description of international services under Section 21(3) of the GST Act.

A) True

B) False

Click for the answer

A) True

A service is considered an international service which is zero-rated (i.e. GST is charged at 0%), if it falls within the provisions under Section 21(3) of the GST Act.

Q2. A supplier issued an invoice to an overseas customer on 1 May 2025. He received payment on 30 May 2025 and exported the goods with all the required documents on 15 Jul 2025. Can he zero-rate the supply of goods?

A) Yes, he can zero-rate the supply as he obtained all the export documents within 60 days of the invoice date

B) No, he cannot zero-rate the supply as he did not obtain all the export documents within 60 days of the invoice date

C) Yes, he can zero-rate the supply as he obtained all the export documents within 60 days of the payment receipt date

D) No, he cannot zero-rate the supply as he did not obtain all the export documents within 60 days of the payment receipt date

Click for the answer

B) No, he cannot zero-rate the supply as he did not obtain all the export documents within 60 days of the invoice date

A supply of goods exported out of Singapore can be zero-rated if the supplier is certain at the time of supply (i.e. earlier of the date the invoice is issued, or payment is received) that:

- the goods supplied have been exported or will be exported, and

- he has or will have the required documents to support zero-rating the supply.

As the goods were exported on 15 Jul 2025 which is more than 60 days from the time of supply (i.e. invoice date of 1 May 2025), the export of goods cannot qualify for zero-rating. The sale of goods has to be standard-rated.

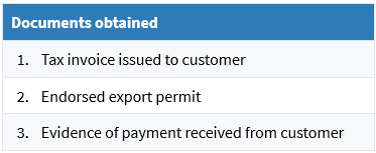

Q3. A supplier has charged his overseas customer GST at the prevailing GST rate on the sale of goods hand-carried out of Changi Airport. He obtained these documents (as stated below) within 60 days from the time of supply.

The supplier refunded the GST amount charged and issued a credit note to the overseas customer 6 months after the time of supply. Can the supplier zero-rate the export of goods?

A) Yes, the export can be zero-rated since the supplier refunded the GST amount to the customer

B) No, the export cannot be zero-rated since the GST refund was not made within 60 days from the time of supply

Click for the answer

B) No, the export cannot be zero-rated since the refund was not made within 60 days from the time of supply

If GST is charged and collected at the prevailing GST rate from the overseas customer at the time of supply, an invoice or tax invoice should be issued for the sale. Upon receipt of the endorsed export permit within 60 days from the time of supply, the charged GST should be refunded to the customer with a credit note issued for the GST refunded.

One of the supporting documents to be obtained within 60 days of the time of supply is the evidence of payment made to the overseas customer for the refund of GST that was previously charged.

Since the refund of GST was made after 60 days from the time of supply, the supplier did not maintain all of the supporting documents to qualify for zero-rating.

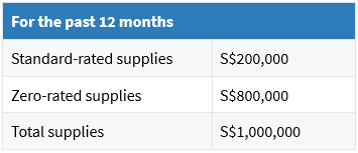

Q4. Company ABC operates an import and export business. Its zero-rated supplies account for 80% of its total supplies. Can Company ABC apply for the Major Exporter Scheme?

A) Yes, its zero-rated supplies account for more than 50% of the total supplies

B) No, the value of its zero-rated supplies is less than S$10 million for the past 12 months

Click for the answer

A) Yes, its zero-rated supplies account for more than 50% of the total supplies

One of the conditions to qualify for the Major Exporter Scheme is that your zero-rated supplies must account for more than 50% of the total supplies, or the value of your zero-rated supplies is more than S$10 million for the past 12 months.

Since Company ABC's zero-rated supplies account for 80% of its total supplies, it satisfies this criterion to apply for the Major Exporter Scheme.