For business owners who are GST-registered, you may be eligible to claim the Goods and Services Tax (GST) incurred for your business purchases and expenses. However, when making your input tax claims, remember that the following expenses cannot be claimed as input tax:

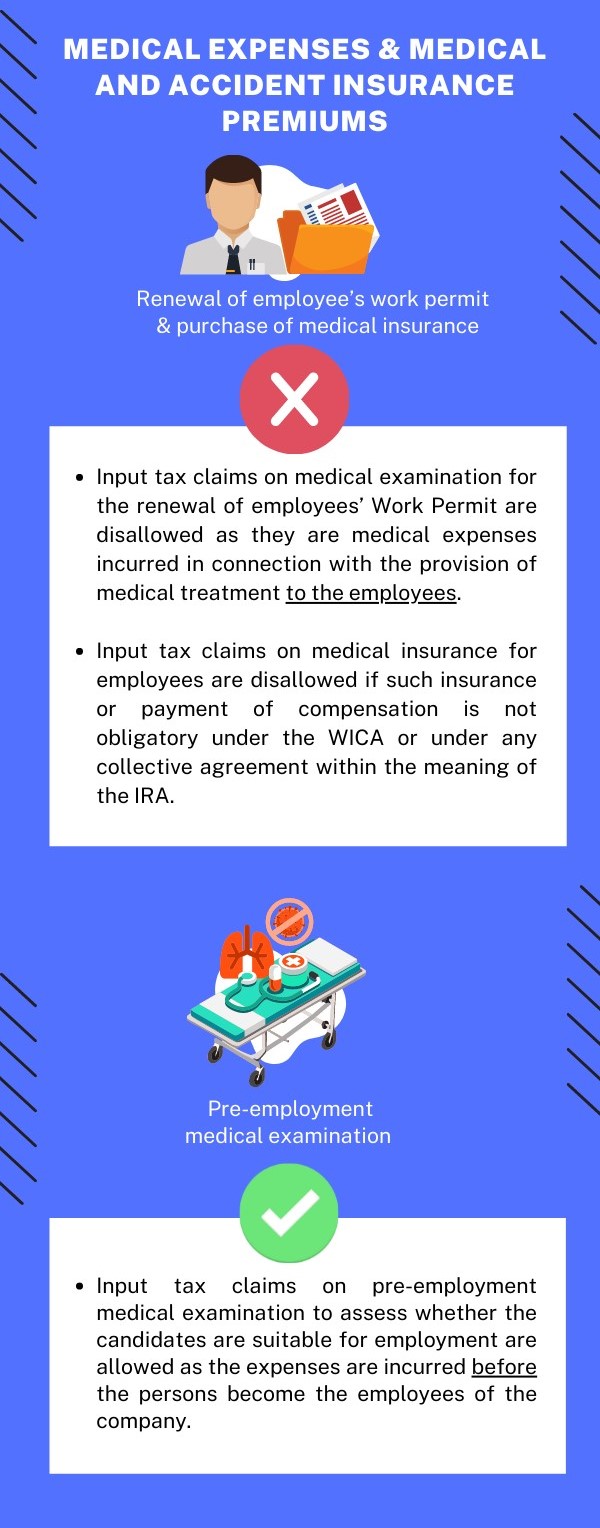

- Medical expenses incurred for your staff unless –

- the expenses are obligatory under the Work Injury Compensation Act (WICA) or under any collective agreement within the meaning of the Industrial Relations Act (IRA); or

- the medical treatment in respect of expenses incurred on or after 1 Oct 2021 is provided in connection with any health risk or requirement arising on account of the nature of the work required of your staff or his work environment; and

- the medical expenses are incurred pursuant to any written law of Singapore concerning the medical treatment or the provision of a medical facility or medical practitioner; or

- the medical treatment is related to COVID-19 and the staff undergoes such medical treatment pursuant to any written advisory (including industry circular) issued by, or posted on the website of the Government or a public authority

- Medical and accident insurance premiums incurred for your staff unless the insurance or payment of compensation is obligatory under the WICA or under any collective agreement within the meaning of the IRA;

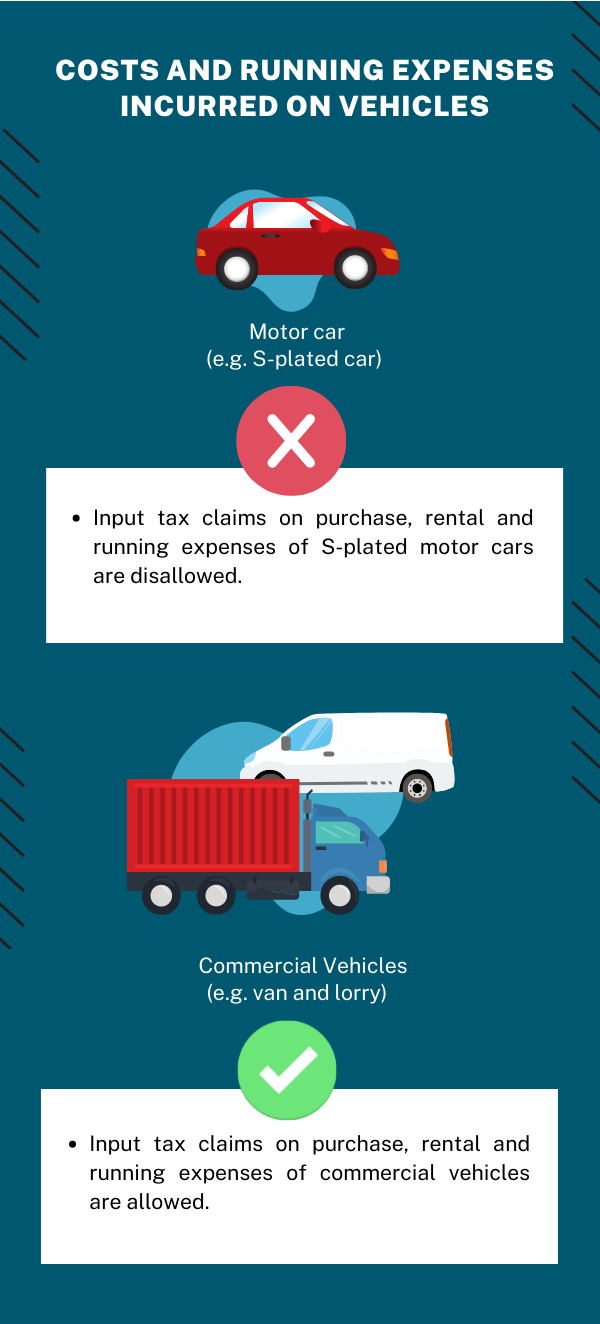

- Costs and running expenses incurred on motor cars that are either:

- registered under the business's or individual's name, or

- hired for business or private use

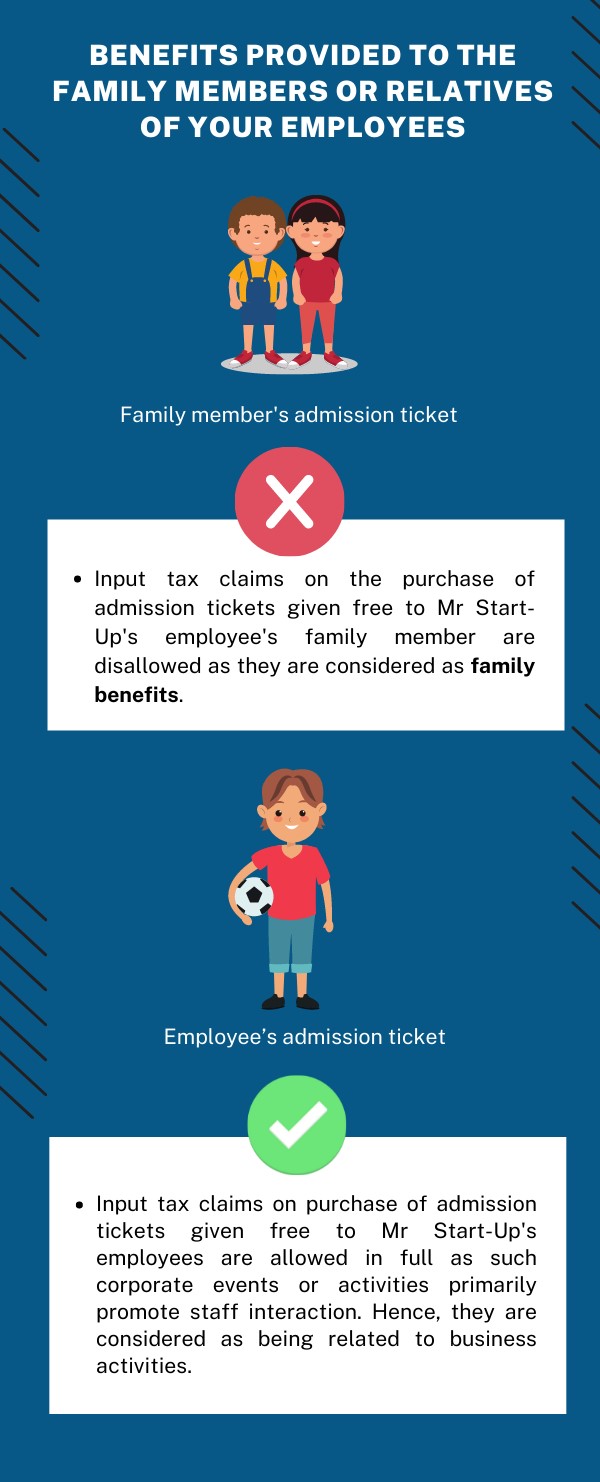

- Benefits provided to family members or relatives of your employees

- Club subscription fees (including transfer fees) charged by sports and recreation clubs; and

- Any transaction involving betting, sweepstakes, lotteries, fruit machines or games of chance

Getting your input tax claims right

If you are not sure how to assess if the input tax claim is allowed, check out our scenario guides below to guide you in avoiding common errors when filing your GST returns.

- Medical expenses & medical and accident insurance premiums

Scenario: Ms Baker sent her employees for a medical examination to renew their work permit and extended the employees’ existing medical insurance. She also sent potential candidates for a medical examination to check whether they were fit for work before employment. She incurred GST on the medical examinations and medical insurance. Is she able to claim GST?

- Costs and running expenses incurred on vehicles

Scenario: As a wholesale distributor of beauty products, Ms Beauty Lover owns a fleet of vans to supply and deliver the goods to the retailers. She also rents motor cars (S-plated cars) for her salespersons to travel to meet retailers at their premises. Other than the running expenses (e.g. season parking fees, petrol, repair and maintenance) of the vans and motor cars, she also incurred GST on the rental of the motor cars. Is Ms Beauty Lover able to claim GST?

- Benefits provided to family members or relatives of your employees

Scenario: To promote staff interaction, Mr Start-Up decided to organise a family day at the zoo for his employees and their family members. He gives each employee 2 tickets free of charge – 1 ticket for his employee and 1 ticket for his employee’s family member. He incurred GST on the purchase of admission tickets. Is Mr Start-Up able to claim GST?

- Club subscription fees (including transfer fees) charged by sports and recreation clubs

Scenario: Mr Start-Up also subscribed to a country club membership where he enjoys full access to the club’s golf and resort facilities (e.g. swimming pools, fitness centre, arcade games room). His sales executives will entertain business clients by playing golf or engaging in other social activities at the country club. He incurred GST on the club subscription fees and other expenses for use of the club facilities. Is Mr Start-Up able to claim GST?

How to correct mistakes in your GST return

Discovered errors in your GST return? You should use the GST F7 calculator (XLSX, 122KB) to see if you can adjust your errors in your next GST return. If you are not able to do so, correct the errors by filing a GST F7 via myTax Portal.

You may qualify for reduced penalties if you voluntarily disclose your errors.