Beware of GST Missing Trader Fraud involving precious metals

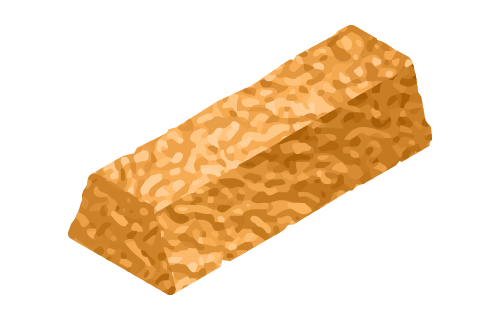

Cast Gold Bar | Cut Gold Bar | Scratched Gold Bar |

|  |  |

Missing Trader

| Buffer

| Bullion Traders, Jewellers and Refiners | ||||||||

|  |  | ||||||||

| Transforms IPM gold bars into scrap gold bars by melting, cutting or defacing them; and sells the scrap gold bars to the Buffer. Charges the Buffer GST but does not remit the GST to IRAS. | Sells the scrap gold bars to the jewellers, bullion traders or refiners. Offsets the GST on the sales with the GST on the purchases. |

|

The Knowledge Principle

Under the Knowledge Principle, you should have known that a supply made to you is a part of an MTF arrangement if:

- The circumstances connected with the supply made to you or with a supply made by you, or both, carried a reasonable risk of the supply being a part of such arrangement; and

- Before making a claim for input tax on the supply made to you, you did not take reasonable steps to ascertain whether the supply was a part of such an arrangement; or

- You took reasonable steps to ascertain whether the supply was part of such arrangement, and

- concluded that the supply was not a part of such arrangement, and the conclusion is not one that a reasonable person would have made;

- were unable to conclude that the supply was not a part of such arrangement; or

- did not make any conclusion as to whether the supply was or was not a part of such arrangement.

- High-value deals offered by newly established supplier, with minimal experience in the industry.

- Very quick turnaround of high-volume transactions, making the business appear unrealistically lucrative.

- Back-to-back purchase to sale arrangement with a fixed gold price between the supplier and customers, making the business practically risk free with little or no exposure to price volatility.

- Out of the norm credit terms. For example, supplier delivers the gold to you first, and only requires you to make payment after you receive the payment from the customer.

- Too good to be true deals recommended by unfamiliar introducer.

- Scrap gold bars in condition or volume that is not ordinarily traded in the market. For example, buying or selling cut or defaced IPM gold bars or cast scrap gold bars in large quantity.

- Supplier/ introducer is evasive when being asked about the source of its gold supply.

- Material changes in the transactions with existing suppliers or customers. For example, significant increase in transaction volume or transaction value, or changes in the nature of goods trade.

- Are your immediate supplier and customer legitimate? Obtain business incorporation details, perform credit checks, request for trade references and verify whether they are credible, and visit their business premises.

- Is the business arrangement valid? Understand whether there are valid business reasons for IPM gold bars to be defaced or cut and sold as scrap gold bars, whether there are reasonable explanations for the high volume and/or low price of the scrap gold bars relative to the market price and demand, whether the absence of price volatility risk is in line with commercial practice, and whether there is any value for you to be part of the back-to-back purchase to sales arrangement when the customer could have purchased the goods directly from the supplier.

- Is the payment arrangement highly favourable? Is there commercial justification for the payment to be made to the supplier only after payment is received from the customer.

- Are the scrap gold bars authentic? Question the source of the scrap gold bars and whether there is a reasonable explanation for them to be defaced IPM gold bars.

- Is the introducer legitimate and credible? Obtain more information on the introducer. For example, his/her experience in the trade, and the reason for him/her to offer you the deals instead of carrying out the deals himself/herself.

- Is there a valid reason for material changes in the transactions? Be alert to unusual changes when transacting with existing suppliers and customers. For example, question whether there is any reasonable explanation for the significant increase in the transaction volume and value.

- MTF masterminds, co-conspirators and syndicate members who participate in MTF arrangements will be liable to an imprisonment of up to 10 years and/or fine of up to $500,000 upon conviction.

- Current or former sole-proprietors, partners or directors of business entities that are used in MTF arrangements will be liable to an imprisonment of up to 1 year and/or a fine of up to $50,000 upon conviction.

Disclosure of Past Mistakes and Reporting of Malpractices

We encourage businesses to immediately disclosed any past tax mistakes or input tax claimed on supplies that were part of an MTF arrangement. We will treat such disclosures as mitigating factors when determining the appropriate measures. You may refer to our webpage on Voluntary Disclosure of Errors for Reduced Penalties for more information on disclosing past mistakes.

Should you encounter or suspect any malpractices, we urge you to step forward and report them via this form. You may refer to our webpage on Reporting Tax Evasion or Fraud for more information.