Getting your business ready for GST rate change

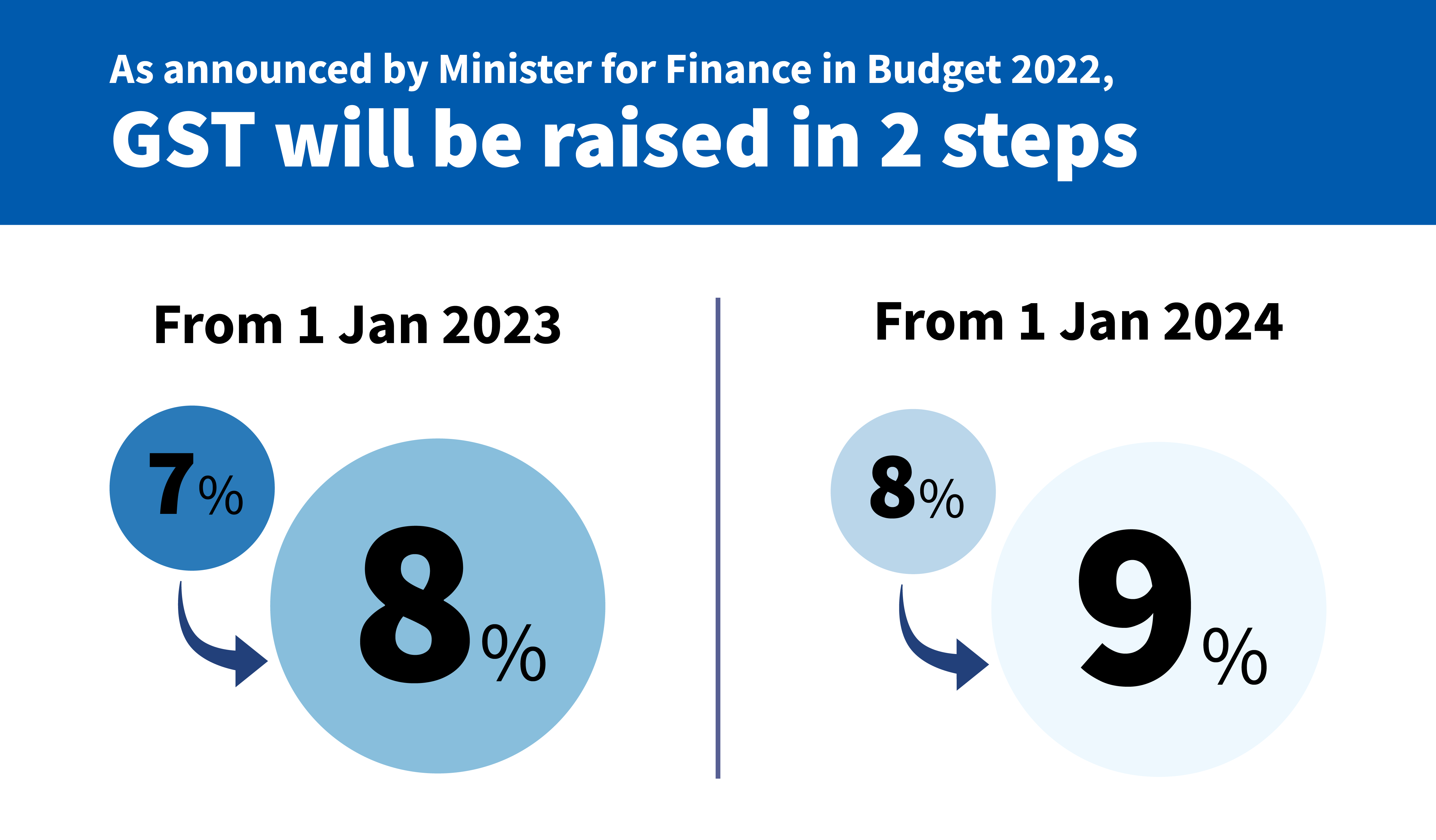

Come 1 Jan 2023, the GST rate will increase from 7% to 8%. All GST-registered businesses are encouraged to start their preparations early for a smooth transition to the new GST rate.

Will my GST-registered business be affected?

Yes, all GST-registered businesses that sell or purchase goods or services that are subject to the standard rate of GST will be affected by the GST rate change. For any standard-rated supplies of goods and services that you make on or after 1 Jan 2023, you must charge GST at 8%. For instance, if you issue an invoice and receive payments for your supply on or after 1 Jan 2023, you must account for GST at 8%.

How can I prepare for the GST rate change?

Prepare early to transit smoothly to the new GST rate to avoid being non-compliant with GST rules. To check if your business is ready for the rate change, you can use the checklist on IRAS' website.

There are 3 main things you need to do:

1. Update your systems to incorporate the new GST rate

Get your systems modified early in readiness for the implementation of GST rate change from 1 Jan 2023. Examples of systems include accounting and invoicing systems, retail management systems, and cash register and receipting systems for point-of-sales (POS) billing.

Some vendors may only require businesses to perform the system updates themselves using available self-help materials online provided by the vendor. For others, the changes may be more complex. Preparing for system changes takes time. Given ample lead time, accounting software vendors are confident in helping you implement the system changes for the GST rate change (Source: Accounting software and POS vendors engagement, Jul 2022). Please check with your in-house IT team or software vendors early on how they can work with you to support a smooth transition. Start now, to avoid penalties being imposed for non-compliance with invoicing rules, price display, and incorrect accounting of GST.

2. Prepare your price displays to reflect the new GST rate

All price displays must show GST-inclusive prices. Price displays include price tags, price lists, advertisements, publicity brochures and websites. Prices that are quoted, whether written or verbal, must be GST-inclusive as the public needs to know upfront the final price that they have to pay.

Price displays should be inclusive of GST at 8% with effect from 1 Jan 2023, 12 a.m. If you are unable to change your price displays overnight, you may display two prices:

• Prices inclusive of GST at 7% applicable before 1 Jan 2023.

• Prices inclusive of GST at 8% with effect from 1 Jan 2023.

3. Understand the GST rate change transitional rules and apply the correct GST rate for sales transactions and reverse charge supplies spanning 1 Jan 2023

Under normal circumstances, you would refer to the time of supply rules to determine when your supply is treated as taking place for GST purposes. GST should be charged at the prevailing rate based on the time of supply rules. If the time of supply is triggered before 1 Jan 2023, you have to charge GST at 7%. If the time of supply is triggered on or after 1 Jan 2023, the GST rate of 8% will apply.

However, for your supplies straddling the date of GST rate change, you will need to consider the transitional rules to determine whether to charge GST at 8% or 7%. For a comprehensive understanding and application of the transitional rules, refer to our e-Tax Guide “

2023 GST Rate Change: A Guide for GST-registered Businesses”. Here are some examples of how the transitional rules are applied.