What is BCRS?

From 1 April 2026, Beverage Container Return Scheme ("BCRS") will be implemented in Singapore. Under the scheme, a 10-cent refundable deposit (“BCRS deposit”) will be payable on each regulated beverage sold. Regulated beverages refer to pre-packaged beverages in plastic and metal containers ranging from 150 millilitres to 3 litres. Consumers will receive a full refund of the deposit by returning the empty container to a designated return point.

The National Environment Agency (“NEA”) has licensed Beverage Container Return Scheme Ltd. (“BCRS Ltd.”) as the scheme operator to design and operate the scheme in Singapore. As the licensed scheme operator, BCRS Ltd. will be responsible for collecting plastic and metal beverage containers for recycling on behalf of all beverage producers in Singapore. More information about the scheme can be found at www.nea.gov.sg/bcrs.

GST treatment of regulated beverages and BCRS deposit

As a supplier of regulated beverages, you will be required to collect the BCRS deposit on top of the beverage price.

1. The BCRS deposit will not be subject to GST as it is a refundable deposit paid over and above the price for the beverage.

2. You must, however, continue to collect and account for GST on your local sale of the beverage.

An example is provided below:

| Bottled mineral water | : $2.00 (inclusive of GST) |

| GST (9%) | : $0.17 (9/109*$2.00) |

| BCRS deposit | : $0.10 (not subject to GST) |

| Total amount payable | : $2.10 |

Invoicing requirements for BCRS deposit

Since BCRS deposit is not subject to GST, you need not include the deposit in your tax invoice or GST receipt issued for the sale of the beverage. However, for price transparency and ease of operations, you are encouraged to include the BCRS deposit in the invoice and receipt issued to your customer for the sale of beverages.

[UPDATED!] BCRS Ltd. will be issuing guidelines on the communication of the BCRS deposit collection to your customers in early 2026.

1. If you choose to issue a tax invoice or simplified tax invoice for BCRS deposit, you should include 2 additional information in the invoice:

(i) A description to identify BCRS deposit as a separate amount on the invoice; and

(ii) Indicate that BCRS deposit is not subject to GST.

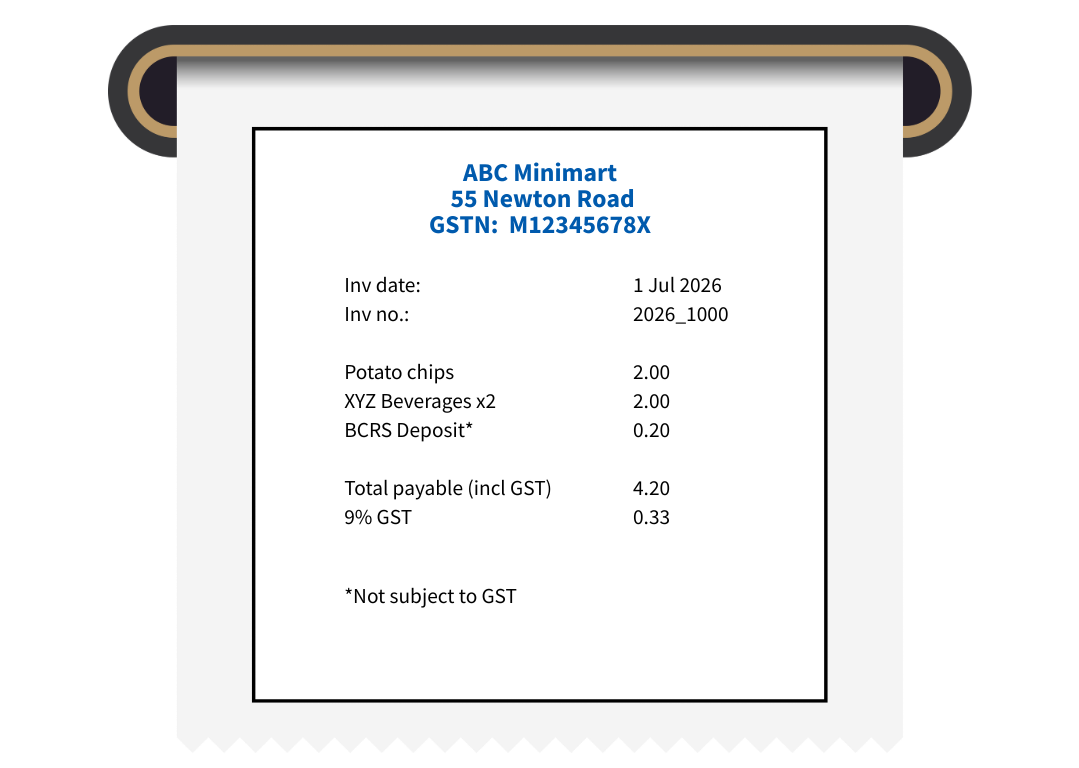

Example of an acceptable simplified tax invoice showing BCRS deposit

Please refer to IRAS’ webpage on GST and BCRS deposit for more examples of tax invoice formats that include BCRS deposit.

Important to-do:

- Update your accounting and point-of-sale systems so that you do not charge GST on the BCRS deposit.

- Separate the amount of BCRS deposit from the other items on your tax invoices and simplified tax invoices. This helps you to properly account for output tax on your beverage sales and enables your GST-registered customers to accurately identify and claim input tax on eligible items.

For more information, you can refer to IRAS’ webpage on GST and BCRS Deposit.