The PIC scheme has expired after the Year of Assessment (YA) 2018. Businesses are not allowed to claim PIC benefits on expenditure incurred after the basis period of YA 2018.

On this page:

From 1 Aug 2016, e-Filing of the PIC cash payout application is compulsory for all PIC cash payout applicants (including companies, partnerships and sole-proprietors). Hardcopy applications for PIC cash payout will not be accepted on or after 1 Aug 2016.

Applying for PIC Cash Payout

Step 1: Authorise an employee or a third party

Your company or partnership has to first authorise an employee, business owner (director or partner) or a third party, such as a tax agent, for 'PIC Cash Payout' in Corppass.

The authorisation is a one-off process and the authorised personnel will be able to make PIC cash payout applications for the company or partnership as long as his/ her authorisation remains valid. For assistance on Corppass set up, refer to the step-by-step guides.

Note: Sole-proprietors do not have to be authorised via Corppass.

Step 2: Prepare information needed to e-File the application and determine the incurred dates for your PIC qualifying expenditure

Before you start e-Filing, get ready the necessary information stated in Essential Information for completing PIC Cash Payout digital service (PDF, 270KB) so that you can complete the application in 1 session. Where applicable, prepare the hire-purchase template and/or Research and Development claim form.

If you have incurred qualifying expenditure before and after 1 Aug 2016, you need to segregate your claims into 2 categories:

- Expenditure incurred before 1 Aug 2016 - 60% cash payout rate

- Expenditure incurred on or after 1 Aug 2016 to the last day of the basis period for YA 2018 (i.e. the last day of your financial year 2017) - 40% cash payout rate

The cash payout cap remains at $100,000 for a YA. Hence, you may wish to prioritise and claim cash payout for expenditure incurred before 1 Aug 2016 first (at 60%), before those incurred on or after 1 Aug 2016 up to the last day of the basis period for YA 2018 (at 40%). You may also refer to the following guidance on determining the dates that expenditure is incurred for PIC cash payout purposes.

The election to convert qualifying expenditure to a cash payout is irrevocable.

Step 3: e-File PIC cash payout application and relevant forms online

The employee/ third party authorised for 'PIC Cash Payout' can log in to mytax.iras.gov.sg to e-File PIC cash payout applications for the company or partnership. A sole-proprietor can log in to mytax.iras.gov.sg directly without any Corppass authorisation.

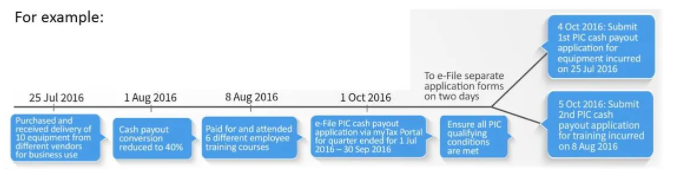

The 'Apply for PIC Cash Payout' digital service only accepts 1 application a day for each quarter or combined quarters of each YA and up to 15 items of expenditure. The minimum qualifying expenditure for each application is $400.

- If you are claiming PIC qualifying expenditure of 15 items or less for 1 YA, you may submit a single PIC cash payout application even if the incurred dates straddle 1 Aug 2016. The PIC cash payout digital service will automatically compute the eligible cash payout rate.

- If your PIC cash payout application consists of more than 15 items for 1 YA, you should submit separate forms on 2 days in the following order to maximise your PIC cash payout conversion cap -

- First application: for expenditure incurred before 1 Aug 2016

- Second application: for expenditure incurred on or after 1 Aug 2016

Tip: You may consolidate the items (e.g. by vendor) and provide a detailed breakdown of the consolidated items and their qualifying costs in the description box.

You can submit your cash payout claim any time after the end of your financial quarter, but not later than the Income Tax Return filing due date for the relevant YA.

The PIC cash payout digital service will not accept any application that is submitted before the end of the financial quarter and you will receive an error message if you make such a submission. You can submit your application only after the end of the financial quarter.

| YA | When to Submit | Relevant Month(s) for Determining 3-Local-Employee Condition |

|---|---|---|

| 2016 to 2018 | Quarterly Applications Not later than the filing due date of Income Tax Return. | Contributes CPF on the Payroll For: See Worked Examples (PDF, 85KB) for YAs 2016 to 2018. |

| 2013 to 2015 | Quarterly Applications Not later than the filing due date of Income Tax Return. | Contributes CPF on the Payroll For: See Worked Examples (PDF, 58KB) for YAs 2013 to 2015. |

You will receive an instant acknowledgement if the PIC cash payout application is transmitted to IRAS successfully. Hence, there is no need to contact IRAS to ascertain if IRAS has received your application.

PIC Cash Payout e-Filing Tips!

| S/N | Common Authorisation/ e-Filing Issue | What You Need To Do |

|---|---|---|

| 1 | Why am I unable to view the 'Apply for PIC Cash Payout' digital service at the top menu bar of myTax Portal? | This is because you have not been authorised in Corppass by the company/ partnership to act for its PIC cash payout matters. For assistance on Corppass set up, refer to the step-by-step guides. |

| 2 | I am authorised for 'Corporate Tax (Filing and Applications)' and/or 'GST (Filing and Applications)' in Corppass. However, I am unable to view the 'PIC Cash Payout' digital service at the top menu bar of myTax Portal. Why is this so? | You must be separately authorised in Corppass by the company/ partnership for 'PIC Cash Payout'. The authorisation for 'PIC Cash Payout' is separate from 'Corporate Tax (Filing and Applications)' and/or 'GST (Filing and Applications)'. |

| 3 | Why am I unable to submit online PIC cash payout application form to IRAS after completing it? | Only persons authorised as an 'Approver' for PIC cash payout matters can submit the application to IRAS. Should you wish to submit the PIC cash payout application form to IRAS, you must arrange for yourself to be authorised as an 'Approver' for 'PIC Cash Payout' in Corppass. |

For assistance with the PIC cash payout e-Filing applications, refer to:

- Step-by-step guide (For Companies/ Partnerships) (PDF, 1.62MB)

- Step-by-step guide (For Tax Agents) (PDF, 1.70MB)

- Step-by-step guide (For Sole-proprietorships) (PDF, 2.1MB)

- FAQs on PIC Cash Payout digital service (PDF, 325KB)

PIC Cash Payout Processing

IRAS strives to disburse the cash payout within 3 months of receiving your complete application*. In most cases, IRAS processes the applications within 6 weeks.

IRAS selects a sample of applications for audit. For cases selected for audit, IRAS will request further details and supporting documents for review. Submit the requested documents in an envelope labelled clearly with:

- 'PIC - Companies' for companies

- 'PIC - Individuals' for sole-proprietorships and partnerships

We strive to complete the review within 3 months from receiving the complete information. The processing time may take up to 6 months, depending on the complexity of each case.

Do note that IRAS may also select PIC applications for further review, even after disbursing the cash payout.

* An application is considered complete if the form and the relevant documents (i.e. the Hire Purchase Template (XLSX, 301KB) and/or the Research and Development (R&D) Claim Form (YA 2018 and before) (PDF, 382KB)) are filled out properly.

Checking the Status of your PIC Cash Payout Application

A person who is authorised for 'PIC Cash Payout' in Corppass can log in to mytax.iras.gov.sg to check the PIC cash payout application status of the company or partnership via the 'View PIC Cash Payout Application Status' digital service.

A sole-proprietor can log in to mytax.iras.gov.sg directly to check the PIC cash payout application status without any Corppass authorisation.

The PIC cash payout application status will be available for viewing within 3 days from the date of submission of your PIC cash payout application. The application status will be shown as 'In Process' until IRAS approves the application. IRAS selects a sample of applications for audit and will call for supporting documents for review. If your application is under audit and you have submitted additional information upon IRAS’ request, the status will continue to show 'In Process' until the audit is completed. This may take up to 6 months, depending on the complexity of each case.

You may view the status of applications made for 2 future YAs, the current YA and the past YA. For example, if you log in on 15 Jun 2016, you can view the status of applications for YAs 2015 to 2018. You will be able to view the status of all applications for these YAs, whether the applications were made via digital services or otherwise.

We encourage you to check your application status via the digital service - this is the quickest and most convenient way, as you will be able to access the digital service anytime.

You may refer to the step-by-step guide (PDF, 500KB) and the FAQs on PIC Cash Payout Application Status digital service (PDF, 126KB) for more information.

FAQs

Applying for Cash Payout

My company is facing difficulties in e-Filing my Cash Payout. Can I get a waiver from e-Filing and submit a hardcopy cash payout application form instead?

From 1 Aug 2016, e-Filing of PIC cash payout applications is compulsory and hardcopy application forms will not be accepted on or after this date. Taxpayers are advised to e-File their PIC cash payout applications early before the filing due date of the Income Tax Return. Refer to our step-by-step user guides for guidance.

My company purchased a total of 30 different PIC qualifying items in YA 2017 and the financial year end is 31 Dec. How and when can I submit the cash payout application for YA 2017?

The PIC cash payout digital services accept only 1 application form (with a maximum of 15 qualifying items) per day.

If you have more than 15 qualifying items and need to e-File more than 1 application, you will need to e-File on different days. Do e-File early as the PIC application can be submitted any time after the end of the quarter or combined quarters, but before the Income Tax Return filing due date.

My business’ financial year ended on 31 Mar 2016 (YA 2017). When can I apply for the cash payout? When will I receive the cash payout?

From YA 2013, a business can apply for cash payout by submitting the PIC cash payout application any time after the end of its financial quarter(s), but not later than the Income Tax Return filing due date of the relevant YA (15 Apr for sole-proprietorship and partnership; 30 Nov for company).

In this case, as your financial year ended on 31 Mar 2016, the financial quarters for YA 2017 are:

| Quarter | From | To |

|---|---|---|

| Q1 | Apr 2015 | Jun 2015 |

| Q2 | Jul 2015 | Sep 2015 |

| Q3 | Oct 2015 | Dec 2015 |

| Q4 | Jan 2016 | Mar 2016 |

You can submit the application for cash payout after the end of each quarter i.e.:

- Q1: Submit in Jul 2015

- Q2: Submit in Oct 2015

- Q3: Submit in Jan 2016

- Q4: Submit in Apr 2016

You can also combine consecutive quarters for your cash payout application, for example, combine Q1 and Q2 and submit 1 application in Oct 2015, after Q2 has ended.

The due date to submit the application(s) for cash payout is 15 Apr 2017 for sole-proprietorship and partnership; and 30 Nov 2017 for company.

If your claim for cash payout is approved, you will generally receive the cash payout within 3 months of receipt of the duly completed PIC cash payout application. For instance, if you are claiming cash payout on qualifying expenditure incurred in Q4 (financial quarter from Jan 2016 to Mar 2016) and have submitted the cash payout application on 15 Apr 2016, the cash payout will generally be made by IRAS by 15 Jul 2016 if your claim is approved.

Do note that IRAS selects a sample of applications for audit. For cases selected for audit, IRAS will request further details and supporting documents for review. We strive to complete the review within 3 months from receiving the complete information. The processing time may take up to 6 months, depending on the complexity of each case.

My business’ financial year ended on 31 Mar 2016 (YA 2017). I made a claim and received my cash payout for qualifying expenditure (items 1 and 2) incurred in the financial quarter from Oct 2015 to Dec 2015. I omitted to make a claim for a qualifying expenditure (item 3) incurred in the same quarter i.e. Oct 2015 to Dec 2015 and want to make a claim for item 3. Can I do it and if so, how?

You can re-submit the cash payout application for the same quarter i.e. Oct 2015 to Dec 2015.

In the application, you should only include claims for the new item i.e. item 3 and not items 1 and 2, which were previously approved. Penalties may be imposed on duplicate claims made.

Alternatively, you can include the claim for item 3 together with your claim for a subsequent quarter in the same financial year, provided you meet the 3-local-employee condition for that subsequent quarter.

I am submitting my company’s Estimated Chargeable Income (ECI) soon. Do I have to submit any forms (for purposes of PIC) together with the ECI?

You do not need to submit the PIC cash payout application together with your company's ECI. If you are claiming the enhanced tax deductions or allowances under PIC, the claim should be made in the tax computation for the relevant YA.

ECI has to be submitted within 3 months from the company's financial year end.

For Sole-Proprietorships

When can I submit my claim for cash payout if I am a sole-proprietor with multiple sole-proprietorships?

A sole-proprietor is only required to submit 1 PIC cash payout application for the multiple sole-proprietorships that have incurred qualifying expenditure. You must submit the application after the financial period of all the businesses have ended.

From YA 2013, businesses can apply for cash payout by submitting the PIC cash payout application after the end of any financial quarter(s) in the business' financial year, but not later than the Income Tax Return filing due date of the relevant YA (15 Apr for sole-proprietorship and partnership).

If I have more than 1 sole-proprietorship, how many applications must I submit?

You only need to submit 1 application for all your sole-proprietorships as the cash payout is capped at the sole-proprietor level. However, separate annexes for claims relating to each individual sole-proprietorship need to be submitted together with the application.

I am not required to file certified statement of accounts for income tax purposes for both my sole-proprietorship and partnership as both businesses have revenue of less than $500,000 each. Do I have to submit certified statement of accounts if I wish to apply for the cash payout?

For the purpose of claiming cash payout, you are required to submit certified statement of accounts by the income tax filing due date of 15 Apr. This is regardless of whether the revenue of the business is less than $500,000.

However, from YA 2013, sole-proprietorships and partnerships opting for cash payout no longer need to submit certified statements of accounts together with their Income Tax Returns.

Receiving the Cash Payout

Will the cash payout be used to offset my tax arrears?

Yes. The cash payout will be used to offset any tax arrears (such as Individual/ Corporate/ GST/ Property Tax) of the business before any remaining amount is paid to the business.

How will the payment of the cash payout be made?

The cash payout is paid to the business which incurred the qualifying expenditure. You can expect the cash payout to be credited into your existing GIRO account (according to IRAS' records) or receive a cheque otherwise.

If you have received the payment via cheque, deposit it into your bank account within 3 months from the date of the cheque.

My business uses different bank accounts for GIRO payment of Income Tax and GST. Which bank account will the cash payout be credited to?

The cash payout will be credited to your Income Tax GIRO account.

What will happen in the event that the GIRO crediting is not successful (e.g. bank account is closed)?

We will send you a cheque for the cash payout within a week of the unsuccessful GIRO payment.

I have misplaced the cheque for the payment of cash payout. What should I do?

You may contact IRAS via [email protected] or 1800 356 8622 (for companies) and [email protected] or 6351 3534 (for sole-proprietorships/ partnerships) for assistance.

Recovery of Cash Payout

Under what circumstances do I have to repay the cash payout?

You are required to own the automation equipment and/or registered IPRs for which the cash payout has been made for at least 1 year from the date of acquisition of the automation equipment and/or filing of the IPR. You are required to own acquired IPRs for at least 5 years from the date of acquisition of the IPR.

Claw-back provisions apply to the cash payout if the minimum ownership requirement is not met.

Cash payout will also be recovered if your design project submitted to DSg is not approved.

Learn more about the claw-back provisions.